Can private finance fix Scotland’s nature crisis?

Restoring nature by luring private finance comes with many risks – and an unknown price tag

By Laurie Macfarlane

15 March 2024

By Laurie Macfarlane

15 March 2024

Two critical questions rest at the heart of the debate around delivering a just transition: who pays, and who wins? Meeting Scotland’s climate targets will require large amounts of new spending and investment. Who funds this, and how the rewards are shared, will be key in determining whether Scotland’s net zero transition is fair and just.

One area where these questions are particularly relevant is how we restore nature. The Scottish Government has committed to increasing woodland creation to 18,000 hectares per year by 2024/25, and restoring 250,000 hectares of degraded peat by 2030. Delivering this has a cost – both in terms of up-front investment and ongoing maintenance.

To date, the Scottish Government has covered a majority of the up-front costs of tree planting and peatland restoration through Forestry Grant Scheme (FCG) and Peatland Action Fund (PAF) grants. Landowners are then able to monetise carbon sequestered by generating carbon credits, which can be sold on carbon markets or used to offset the landowners' own emissions.

Under this approach however, Scotland has repeatedly failed to meet its woodland creation and peatland restoration targets. To scale up delivery, the Scottish Government has sought to attract responsible private investment into Scotland’s natural capital. The idea that luring private finance is essential – and indeed the only viable pathway – to meeting Scotland’s nature targets has quickly become accepted wisdom. Scotland is not alone: governments across the world have taken steps to turn nature into a new investable asset class.

For cash-strapped governments, asking private finance to fund nature restoration might seem like an appealing option. But it comes with many risks – and an unknown price tag.

The missing profits

At first glance, attracting private investment into nature restoration might seem like a no brainer. We need to invest in nature, and the fiscal outlook is challenging. Private finance provides loans to many other businesses, so why not nature restoration?

The first problem is that under current market conditions, restoring nature is not a particularly profitable activity. Private investors are not charities: they will only invest if they believe they can generate a commercial rate of return. Delivering woodland creation or peatland restoration involves providing up-front investment in order to receive uncertain income from carbon credits in the future. At present however, carbon prices are not high enough to generate commercial returns from nature restoration alone. As a recent paper by the Scottish Environment, Food and Agriculture Research Institutions (SEFARI) Special Advisory Group notes: “At current carbon prices, many woodland and peatland projects may not be financially viable for land managers based solely on carbon finance.”

Although there has been a dramatic rise in the number of investors buying rural land for carbon offsetting purposes in recent years, the expected returns from these investments are predicated on the acquisition of land, which investors believe will substantially increase in value. In turn, the arrival of so-called ‘green lairds’ has pushed up rural land prices, creating widespread concerns that the ‘natural capital’ agenda could exacerbate long standing inequalities in Scotland’s land market.

In response to this, the Scottish Government has urged investors to “consider whether ownership of land is necessary”, and instead consider opportunities for “management agreements and collaboration/partnerships with communities that can deliver wider social and economic benefit.” While this sounds sensible in theory, the problem is that nature restoration is not particularly profitable when acquiring land is not part of the deal. This should not be surprising: nature is a public good with large social and environmental externalities, and basic economic theory tells us that private markets are not very effective at providing public goods. This is why governments currently provide grants to subsidise activities like woodland creation and peatland restoration. Without them, these activities simply would not happen.

"Nature is a public good with large social and environmental externalities"

But if the goal is to attract private finance, the availability of generous public grants presents a problem. Why would landowners take out a commercial loan to fund these activities when they can get a government grant for free? This is often referred to as an example of public funds ‘crowding out’ private investment. Herein lies the problem.

The Scottish Government wants to attract private investment into an activity that is not viable without public subsidy. But the existence of these subsidies is ‘crowding out’ the investment it wants to attract. Under these circumstances, it is unlikely that the private finance the Scottish Government wants to attract will materialise. The only way to square this awkward circle is to change the distribution of risks and rewards in the market – and this means changing the subsidy system.

De-risking to the rescue

In 2023 the Scottish Government commissioned consultancy firm Finance Earth to explore ways to mobilise private investment in nature. The paper acknowledges that “at current market carbon prices, peatland restoration projects are not viable without partial (and typically substantial) grant funding.” It also argues that the current subsidy regime is stifling private investment, noting that “full capital grants from public funding may serve to unnecessarily crowd-out private finance while not providing support for ongoing project maintenance costs.” To address this, the paper proposes replacing the current suite of up-front capital grants with a new subsidy aimed at ‘de-risking’ private finance. De-risking typically involves the state bearing some of the risk associated with private investment to make returns more attractive for investors.

The model proposed by Finance Earth comprises three key elements. The first of these relates to the creation of a £50m Scottish Carbon Fund (SCF) – a new investment vehicle seeded with public and private money to invest in nature restoration projects. Under the proposed approach, the SCF would provide project developers with finance to cover up-front costs associated with nature restoration. Financial returns would then be paid to the SCF once verified carbon credits are sold. In order to de-risk the SCF for private investors, the paper recommends that the Scottish Government provides ‘first-loss’ capital to the fund. In practice, this means that were the fund to make a financial loss, the Scottish Government’s capital would be wiped out first, shielding private investors from losses. While the paper primarily focuses on peatland restoration, it suggests that the SCF’s mandate should be expanded to woodland creation.

The Finance Earth paper proposes that SCF should be accompanied by a Price Floor Guarantee (PFG). This mechanism would involve the Scottish Government guaranteeing a minimum price for carbon, and effectively paying project developers for any revenue shortfall if prices fall below this minimum. As such, the PFG is intended to significantly reduce the downside risk for developers and investors, instead transferring this risk onto the public balance sheet. As the paper notes: “the price floor acts to remove the risk of most pessimistic outcomes (‘downside’) while still providing the opportunity for projects to benefit in upside scenarios.”

With up-front capital costs now being covered by the SCF, the paper proposes that capital grants should be replaced with ongoing ‘operating payments’. These represent annual public grants paid to developers to help cover project costs (including investor returns). The paper also notes that a mixed approach could be taken, whereby developers receive smaller up-front capital grants as well as ongoing operating payments.

Far from private finance helping to sweep away public subsidies, the model involves the Scottish Government subsiding private investors in three separate ways -– a ‘first-loss’ investment in the SCF; compensating revenue shortfalls if prices fall below PFG; and paying annual operating payments. As the report notes, all these mechanisms together “play a key role in directly de-risking investors.”

Shaky foundations

The case for attracting private finance into nature is typically predicated on a number of key assumptions. The first is that the cost of meeting Scotland’s nature targets is too large to be met by the taxpayer. As the Finance Earth paper notes:

“Public funding alone will not be sufficient to meet the targeted nature-related outcomes, with the financing gap estimated at up to £20 billion over the current decade. Private capital will need to be leveraged to close this financing gap.”

The £20bn figure comes from a 2021 report published by the Green Finance Institute, and has been quoted extensively by government ministers and public bodies. However, analysis published by Community Land Scotland and The Forest Policy Group has identified significant problems with the calculation of the £20bn figure. The majority of the ‘gap’ is accounted for by the cost of first acquiring land before undertaking nature restoration. However, land acquisition is not a prerequisite for nature restoration, as restoring nature does not need to involve a transfer in land ownership. Indeed, many existing landowners across Scotland are delivering woodland creation. Although Finance Earth considered whether the SCF should acquire land for restoration projects, it ultimately concluded that a leasehold model should be adopted to reduce the “negative impacts associated with “green lairds.”

Once the cost of land acquisition is removed, the resulting figure is considerably smaller. While the exact ‘finance gap’ remains unknown, Future Economy Scotland has previously estimated that it could be as little as £118m per year, which amounts to around 0.2% of the Scottish Government’s annual budget. This is not to say that this is the correct ‘gap’ – it is simply to highlight that £20bn and £118m per year are worlds apart. If the gap is really in the tens of billions, there would be little choice but to attract private finance. However, if the gap is in the hundreds of millions per year, it would not be impossible to fund this through public spending – particularly given the large scope for reforming taxation and subsidies in Scotland.

Implicit in the case for attracting private finance is the presumption that finance is the key bottleneck to meeting Scotland’s nature targets. But based on the available data it is not clear that this is the case. As noted above, today the majority of costs associated with woodland creation and peatland restoration are covered by public grants. However, in recent years the available grant funding has not been fully utilised. Over the past two years, the budget for woodland grants was underspent by £30m, while the budget for peatland grants was underspent by £20m.

The fact that existing grant funding is not being claimed indicates that many important barriers are not only financial – but also practical (for example in relation to capacity, uncertainty or risk-aversion). If nature restoration is not happening fast enough when projects can access grants for free, it is not clear why replacing grants with commercial loans will increase take up. In contrast, by introducing new costs and complexity into projects, it could conceivably have the opposite effect.

Socialising risks, privatising rewards

Another reason often cited for luring private finance into nature is that it would ease the burden on the public finances. As highlighted in the Finance Earth report, the Scottish Government is keen to expand carbon markets as a means to “reduce dependence on public funds.” Meanwhile, NatureScot, Scotland’s nature agency, has stated that the £2 billion private finance pilot it launched in in March 2023 will help to ease pressure on the public finances, noting that:

“In this new model, we will use an increasing amount of responsible private investment to pay for new woodland, reducing the burden on public finances and increasing the amount of woodland that can be created.”

However, such claims are predicated on the idea that increasing private investment would reduce the need for public subsidy. Again, it is not clear that this is the case. As noted above, the Finance Earth model involves the Scottish Government subsidising nature restoration in three separate ways -– a SCF, PFG and annual operating payments. This would transfer a large amount of risk away from investors and developers and onto the public balance sheet, which could generate significant costs.

The paper suggests that the Scottish Government could contribute £10m of ‘first-loss’ capital into the SCF, and that the ‘operating payments’ should match the value of the current suite of capital grants (in net present value terms). These measures alone would match the public cost of the system operating today.

However, the most risky – and potentially expensive – part of this model relates to the PFG. In guaranteeing a minimum price for carbon, and committing to cover any revenue shortfall if prices fall below this, the Scottish Government would assume significant contingent liabilities. As carbon prices are determined by global market forces, the scale of this liability would be subject to considerable risk and uncertainty, and outside the Scottish Government’s control. Although global carbon prices increased in 2021 and 2022, they have slumped dramatically over the past year. The future trajectory of carbon prices is impossible to predict, and subject to a wide range of economic, political, and environmental forces.

In practice, introducing a de-risking mechanism such as a PFG amounts to placing a large taxpayer-funded bet on volatile carbon prices. If prices rise significantly, the Scottish Government would not need to underwrite revenues through the PFG. But if prices remain low or fall further, the Scottish Government may have to pay out large sums of money to maintain the price floor. Given the Scottish Government's limited borrowing powers, this may have to come at the expense of spending on public services.

"Introducing de-risking amounts to placing a large taxpayer-funded bet on volatile carbon prices"

The paper notes that the price floor should be guaranteed until at least 2050, but that extending the PFG beyond 2050 would “improve developer confidence in the long-term economic viability of the project.” As such, pursuing this model would tie the Scottish Government’s hands financially for at least 25 years, which would create significant uncertainty for its budget. It remains unclear how these contingent liabilities would be managed under the constraints of the existing devolved fiscal framework, or if the Scottish Government has the powers to enter into them.

As such, it is far from clear that de-risking private finance would ease the burden on the public finances. In practice, it could end up being more expensive and complex than direct public investment – while adding significant risk and uncertainty to Scotland’s public finances. As Scotland found out by embracing private finance initiative (PFI) contracts for infrastructure projects, luring private finance to pay for public goods may reduce up-front public expenditure, but it can end up being much more expensive in the longer term.

Heads they win, tails we lose

Beyond creating considerable liabilities for the state, luring private finance introduces new costs and risks into restoration projects. The Finance Earth paper compares the costs associated with a peatland restoration project under two scenarios – one that attracts private investment through the de-risking model outlined above, and one funded by up-front capital grants. Due to the need to pay investor returns, the lifetime costs of the de-risking project are more than 30% higher than the project without private finance. These returns represent additional costs that need to be recovered before the project can break even.

Ordinarily under capitalism, returns are paid to compensate investors for the risks associated with the capital they have provided. But under the proposed model, many of the risks investors face are socialised. To illustrate this, it is useful to consider two scenarios. In the first scenario, carbon prices stay above the price floor, meaning the Scottish Government does not need to pay out through the PFG. It does however still provide annual ‘operating payments’ to the project, which combined with carbon credit sales are sufficient to cover the project’s costs, meaning that investors get paid returns as expected.

In the second scenario, carbon prices fall below the price floor. In this case, the Scottish Government would buy carbon credits at the price floor, maintaining revenues above what market prices would deliver. It would also still provide ongoing operating payments, as in the first scenario. Under this scenario, the Scottish Government would now be providing a large proportion of the project’s revenue, at considerable public expense. Although in the first instance this protects the revenue of the developer, a large proportion of this would then be used to repay borrowed finance, meaning that once again investors get paid.

In the unlikely event that the PFG and operating payments were not sufficient to enable the project to meet its investor repayments, the investors in the SCF would face a financial loss. However, due to the Scottish Government’s ‘first-loss’ capital in the SCF, it would be the public balance sheet that would absorb the loss in the first instance. In other words: the Scottish Government is bearing virtually all the risk in every stage of the project, whereas private investors reap the rewards – regardless of whether carbon prices rise or fall. In both cases, investor profits are entirely dependent on the existence of a web of public subsidies, and are therefore somewhat artificial. This amounts to a clear case of “heads they win, tails we lose.”

If the Scottish Government was willing and able to bear almost all of the risk associated with nature projects, and support a price floor with public budgets, then the point of attracting private investors remains unclear. All this does is introduce significant new costs into the system – and these costs can only be met either through larger public subsidies, or by reducing project developer’s profit. Without this extensive de-risking however, private finance would likely not invest.

"Investor profits are entirely dependent on the existence of a web of public subsidies"

The point of this comparison is not to say that the current system is the optimal model. Landowners often receive grants with few strings attached, and it is unclear that some activities, such as coniferous commercial tree planting, still merit public subsidy at all, as the Royal Society of Edinburgh has highlighted. Moreover, there is evidence that the current laissez faire approach to carbon offsetting may be undermining progress towards the more urgent task of reducing direct emissions.

As such, there is considerable scope to reform the existing investment model to improve incentives, increase investment and deliver better value for money, which Future Economy Scotland will be exploring over the coming months. Crucially however, any subsidies that are paid should be conditional on meeting robust public interest objectives.

One way or another, the need for public subsidy cannot be avoided. The question is: how should subsidies be structured, and whose interests should they serve?

A just transition?

Scotland is not just committed to achieving net zero – it is committed to delivering a just transition. As such, the focus should not just be on mobilising investment, but doing so in a way that shares costs and benefits fairly. As the Interim Principles for Responsible Investment in Natural Capital state:

“Investment in and use of Scotland’s natural capital should create benefits that are shared between public, private and community interests, contributing to a just transition.”

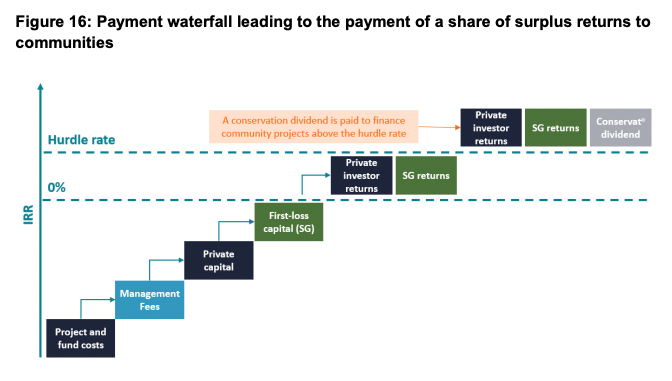

How does de-risking weigh up against these goals? The Finance Earth paper discusses the potential to introduce ‘conservation dividend’, which would be payable to communities once the SCF’s returns exceed a predefined ‘hurdle rate’. Above the level, a proportion of the fund’s returns would be paid to communities in the form of a donation paid to local groups and charities.

As can be seen from the diagram below however, communities come last in the pecking order to receive any benefits. Only after costs have been covered and all investors have been remunerated would communities have the chance to receive a ‘conservation dividend’ – and only if returns significantly exceed expectations. However, the report stresses that community benefits are likely to be minimal for the foreseeable future, stating that: “expectations that a community benefit mechanism could leverage large amounts of money for communities must be carefully managed.” Due to low carbon prices, the report warns that surpluses generated in the early years of the project are “likely to be limited.” In practice, any surpluses that are generated will be reliant on the existence of public subsidies.

Some may argue that this could be addressed by strengthening community sharing mechanisms. However, the more emphasis that is placed on sharing benefits with communities, the less attractive the investment will be to private investors. Investors operate in a global market, and invest wherever offers the most attractive returns. Why would they invest in Scotland if they have to sacrifice a large portion of their returns to communities, when they can invest elsewhere and reap the full rewards?

As such, there is an inherent tension between de-risking private finance on the one hand, and delivering a just transition on the other – particularly when the underlying activity involved is not profitable. In practice, de-risking involves socialising risks, privatising rewards and marginalising communities. Some may think this is a price worth paying if it helps Scotland meet its nature targets. That may or may not be the case, depending on one’s priorities and values. But we should not pretend this approach amounts to “sharing benefits fairly between public, private and community interests”.

"De-risking involves socialising risks, privatising rewards and marginalising communities"

Back to the drawing board

Private finance has a crucial role to play in delivering Scotland’s net zero transition – whether that is to scale up renewable energy or nurture new green technologies. But a key part of ensuring the transition is ‘just’ is knowing when private finance is appropriate, and knowing when it isn’t. With low financial returns and large social and environmental externalities, nature restoration is an awkward bedfellow for private finance.

Despite this, in Scotland the idea that private finance is needed to restore nature has been promoted with relatively little scrutiny. In practice however, the case for doing so often rests on shaky foundations. While more money is likely needed, the claim that the ‘nature finance gap’ is £20bn is a significant over-estimation, and overlooks the non-financial barriers that are holding back investment. Although private finance is often presented as an alternative to public funding, enticing it would require creating a complex web of new subsidies. Far from easing the pressure on the public finances, this could end up being more expensive and uncertain than direct public investment. And crucially, it would distribute risks and rewards in a way that is hard to reconcile with the principles of a just transition.

Although the assessment in this blog has focused on a specific model proposed to the Scottish Government by Finance Earth (which has not yet been implemented) the issues highlighted are likely to all apply to all models that aim to de-risk private finance. While de-risking should certainly be considered as one potential solution, this should be weighed up against alternative approaches. We therefore recommend that the Scottish Government:

- Undertakes detailed analysis to assess the true scale of nature finance gap in Scotland, acknowledging that most nature restoration is already funded from public grants, and that land does not need to be acquired for restoration to take place.

- Conducts a robust appraisal of different private investment models, including the subsidies that would be required to sustain them; their potential impact on the public finances; and their alignment with just transition principles.

- Assesses the costs and benefits of private-finance led models against an alternative public and community-led approach, funded by reforming taxation and subsidies, potentially with support from the Scottish National Investment Bank.

- Reviews the extent to which carbon offsetting is diverting capital away from investment in emissions reduction, and assess whether credits generated in Scotland are delivering carbon sequestration that is genuinely additional.

Future Economy Scotland will be exploring these issues in more detail in the coming months.